THURSDAY, AUGUST 14, 2025

Lok Sabha passes Finance Bill; tax benefits for debt mutual funds removed

Published on Mar 24, 2023

By PTI

Share

In a relief to taxpayers opting for deductions and exemption-free new tax regime, individuals earning marginally higher income than no-tax ceiling of Rs 7 lakh will continue to pay nil tax.

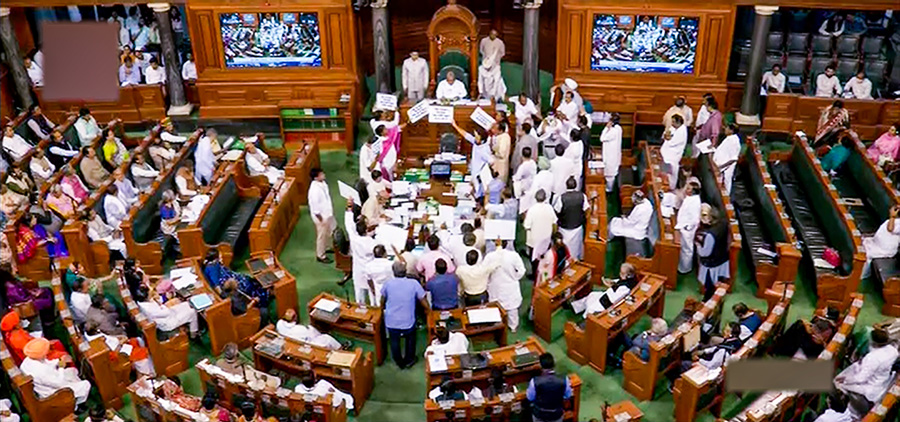

NEW DELHI: The Lok Sabha on Friday approved The Finance Bill 2023 with 64 official amendments including providing tax relief to some taxpayers opting for new tax regime, and removing long-term tax benefit for debt mutual funds to bring them at par with other interest earning instruments.

[bsa_pro_ad_space id=1]Under the new tax regime with effect from April 1, if a taxpayer has an annual income of INR 7 lakh s/he pays no tax. But if s/he has income of INR 7,00,100 s/he pays tax of INR 25,010. Thus an additional income of INR 100 leads to tax of INR 25,010.

The amendment provides that the tax payable should not be more than the income that exceeds INR 7 lakh. This means, an individual having income up to INR 7,27,700 could stand to benefit from this marginal relief.

Other amendments include raising the tax rate on royalty and fee for technical services from 10 per cent to 20 per cent.

The Finance Bill, which includes tax proposals for the fiscal year beginning April 1, was passed without a discussion as parliament continued to remain stalled over demands for a probe into allegations against the Adani group.

Lok Sabha, which had on Thursday approved INR 45 lakh-crore Budget for 2023-24 fiscal in just 9 minutes, passed the Finance Bill amid placards holding opposition MPs shouting slogans from the well of the House.

Finance minister Nirmala Sitharaman moved the Bill and the 64 amendments which were all approved by voice vote.

These will now go to Rajya Sabha and will become law once the President gives assent.

From April 1, investments in debt mutual funds will be taxed as short-term capital gains, stripping investors of the long-term tax benefits that made such investments popular.

Currently, investors in debt funds pay income tax on capital gains according to the income tax slab for a holding period of three years. After three years these funds pay either 20 per cent with indexation benefits or 10 per cent without indexation.

After the amendment, such gains from transfer of units of specified mutual funds will be treated as short term and taxed at slab rates.

This is in addition to taxation of market linked debenture proposed in the original bill.

Specified mutual funds have been defined to include funds where not more than 35 per cent of proceeds is invested in shares of domestic companies. This may include debt mutual funds and gold ETFs where investment in domestic companies is less than 35 per cent of proceeds of the fund.

The move will bring taxation of such mutual funds on par with bank deposits which are taxed at slab rates.

Finance secretary T V Somanathan said the move was aimed at bringing parity with instruments which are of a similar nature.

The government in 2014 had changed the taxation of debt mutual funds (period of holding for short term gains was increased to 3 years and tax rates were increased to 20 per cent).

Also, credit card payments for foreign travel will be brought under the purview of the Liberalised Remittance Scheme (LRS) of the Reserve Bank to ensure that such expenses do not escape TCS (Tax Collection at Source).

The Union Budget 2023 proposed a TCS for foreign outward remittance under LRS other than for education and medical purposes of 20 per cent applicable from July 1, 2023. Before this proposal, the TCS of 5 per cent was applicable on foreign outward remittances above INR 7 lakh.

Tax Collected at Source (TCS) is an income tax, collected by the seller of specified goods, from the buyer. TCS is a concept where a person selling specific items is liable to collect tax from a buyer at a prescribed rate and deposit the same with the government.

The LRS, introduced in 2004, initially permitted outflow of USD 25,000. The LRS limit has been revised in stages consistent with prevailing macro and micro economic conditions.

LRS permits Indians to freely remit up to USD 250,000 (about INR 2.05 crore) per financial year for current or capital account transactions or a combination of both. Any remittance exceeding this limit requires prior permission from the RBI.

Moving the Bill, Sitharaman also announced a committee under the finance secretary to look into pension issues of government employees.

"I propose to set up a committee under the finance secretary to look into the issue of pensions and evolve an approach which addresses the needs of employees while maintaining fiscal prudence to protect common citizens," she said. "The approach will be designed for adoption by both the central government and state governments."

The move comes in the backdrop of several non-BJP states deciding to revert to the DA-linked Old Pension Scheme (OPS) and also employee organisations in some other states raising demand for the same.

The state governments of Rajasthan, Chhattisgarh, Jharkhand, Punjab and Himachal Pradesh have informed the Centre about their decision to revert to the Old Pension Scheme and have requested a refund of corpus accumulated under the NPS.

With the increase in tax rate on royalty and fee for technical services, foreign companies will be required to avail tax treaty shelter to reduce the withholding tax rate.

The proposal to tax the income other than interest, dividend, rent and capital gains, by unit holders of REIT/InVIT has been further amended in the latest round of changes in the Finance Bill.

The government has allowed the benefit of cost against the return of capital component for the unit holders and the tax exemption has been extended to other income arising for sovereign wealth funds/pension funds as unit holders of business trusts.

Also, an amendment approved provides for setting up of the GST Tribunal, which is expected to help streamline pending litigations.

As of December 31, 2022, assets under management for debt oriented products stood at INR 12.42 lakh crore.

MUDRA loans for micro units/enterprises setup under Joint Liability Group (JLG) framework (individually or jointly) are now eligible for guarantee coverage under Credit Guarantee Fund for Micro Units (CGFMU) as per the amended Finance Bill.

Finance Bill proposed to tax distribution from business trust which has income from other sources at applicable rate. This is now proposed to be treated as return of capital i.e. reduction from cost of acquisition, till the cost at which the unit was issued.

However, any amount in excess of the issue price would be taxable as income. Thus, the change would benefit the unitholders vis a vis the earlier proposal.

The amended Finance Bill also deferred the angel tax to April 1, 2024. Exclusions, as already provided to domestic venture capital funds etc, shall also be considered for similar overseas entities.

Two other key changes proposed in the Finance Bill are in relation to taxation of Business Trusts. The government has allowed the benefit of cost against the return of capital component for the unitholders and the tax exemption has been extended to other income arising for sovereign wealth funds/pension funds as unitholders of business trusts, Naveen Aggarwal, Partner, Tax, KPMG in India, said.

As per the Budget proposals, capital gains earned on redemption of market linked debentures (MLDs) would be deemed to be treated as short-term capital gains taxable at slab rates without any indexation benefit, irrespective of the holding period.

As the Finance Act, specified mutual funds where at least 65 per cent investment are in equity shares of domestic companies are also included in the scope of the above deeming provision (along with MLDs), Alok Agrawal, Partner, Deloitte India.

Sitharaman said one amendment is for the GST Council which is establishing the Tribunal.

The amendments proposed in Section 109 of the CGST Act would not merely help the government in setting up of GST tribunals in a time-bound manner but would also enable the Principle Bench to take certain important decisions such as distribution of cases amongst the state benches, referring of case to other members in case of difference in views within the same bench or otherwise, etc.

This would help in streamlining the litigation process, Saurabh Agarwal, Tax Partner, EY said.

Also, Securities Transaction Tax (STT) on options sale has been hiked to INR 2,100 on a turnover of INR 1 crore from INR 1,700 earlier.

Nagaland Districts